I’m thinking about a setup where growth is broadly flat, inflation remains elevated, central banks stay on the sidelines, and credit spreads widen modestly. It’s an uncomfortable mix: not weak enough to force a policy response, but not strong enough to dismiss inflation as the healthy byproduct of robust growth.

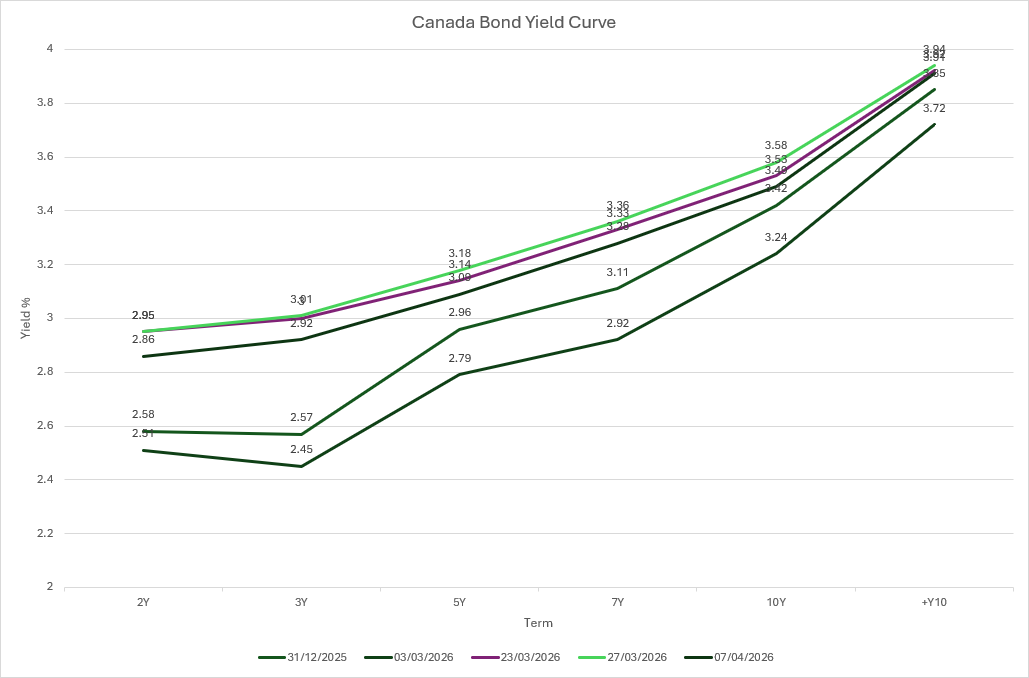

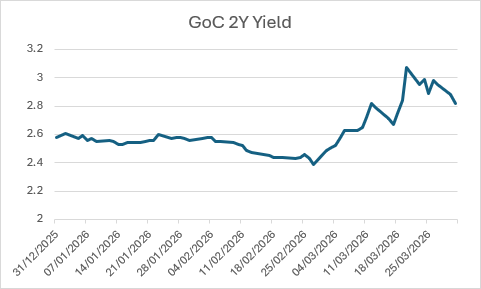

Earlier in the year, bond markets were relatively constructive. Through January and much of February, yields ground lower in an orderly fashion as investors leaned into slower growth and the possibility of eventual easing. Duration was rewarded, and the curve remained positively sloped, cautious but not alarmed.

That tone shifted toward the end of February. Geopolitical risk, particularly around Iran, and the associated rise in oil prices, forced a reassessment. We went from a bond-friendly grind with lower yields in Jan–Feb to a war- and oil-driven bear move from late February into mid-March, with the front end giving back more than the long end and the 2s10s curve flattening by roughly 10–15 bps.

In this context, the long end reflects competing forces: inflation risk pushing term premia higher, while uninspiring growth limits how far long yields can run. The curve remains upward sloping, but less forgiving.

With moderate widening of the credit spread, all-in yields are improving, but the margin for error is thinner. This environment rewards selectivity, disciplined duration management, and balance sheet quality, rather than broad beta exposure.

Curious how others are reading curve dynamics in this “wait and see” world.