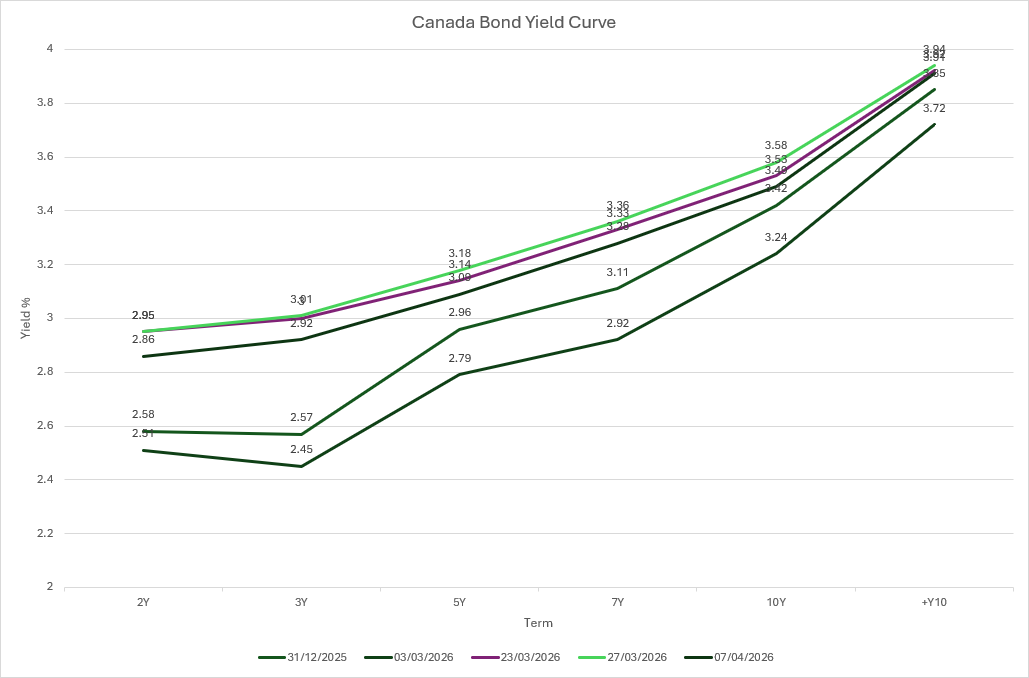

Following the March FOMC and Bank of Canada meetings, central banks remain on hold, but markets haven’t waited. Front-end yields have continued to rise, reflecting not just geopolitical risks and higher energy prices, but also rebuilt inflation risk premia, reduced confidence in near-term easing, and ongoing fiscal uncertainty.

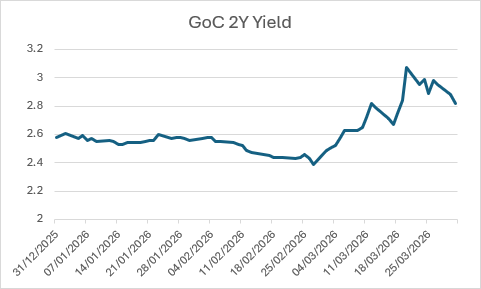

The clearest signal has come from the U.S. 2‑year, where markets have materially repriced the expected policy path since late February. Sticky inflation, heavy issuance, and geopolitical risk have combined to keep short‑term rates elevated, even as growth momentum softens.

Canada has followed suit. Canadian 2‑year yields have moved higher, broadly tracking the U.S. sell‑off, with the Canada–U.S. front‑end spread widening modestly. While the Bank of Canada may be closer to holding than hiking, investors continue to demand compensation for inflation risk and global spillovers, underscoring how interconnected rate markets remain.

Looking ahead, resolution of the Iran conflict could come sooner rather than later, but normalization in energy markets and supply chains may take longer, keeping inflation risks alive in the near term. My base case is that the front‑end yields peak before fall, as slowing growth and easing labour‑market pressures eventually reassert themselves. Volatility may persist, but today’s higher short‑term yields are already improving forward return potential.

For investors, this environment reinforces the importance of balance and selectivity. Higher all‑in yields help, but only if policy uncertainty begins to fade. Interested to hear how others are thinking about front‑end rates and portfolio positioning.