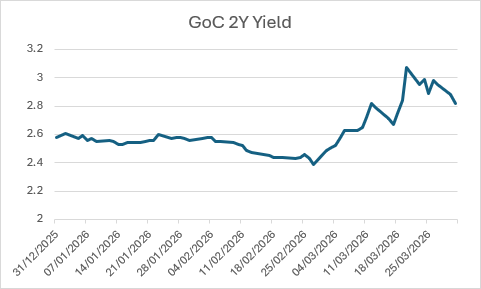

The attached chart captures a quiet but important shift in Canadian rates this year.

Coming into 2026, yields drifted lower in an orderly way, led by the front end, as markets leaned toward slower growth and a patient Bank of Canada. The curve stayed positively sloped, and duration was rewarded. That changed in late February. Geopolitical escalation and higher energy prices triggered a reassessment: yields moved higher, volatility picked up, and the curve flattened as inflation risk re‑entered the pricing.

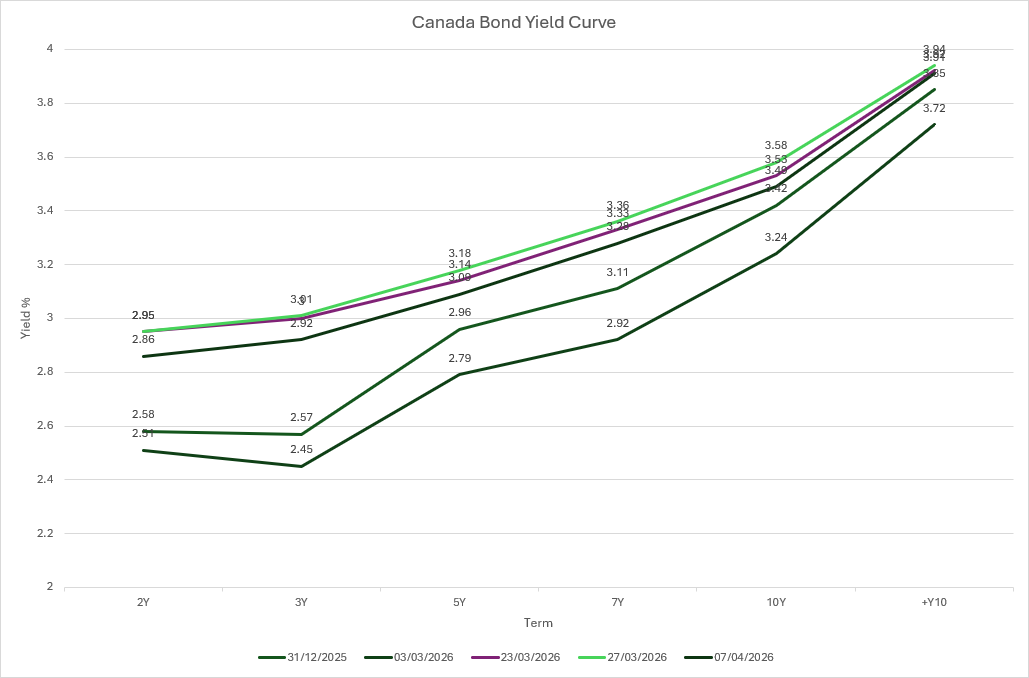

More recently, the curve has stabilized, but at higher levels, especially beyond the belly. A credible ceasefire involving the U.S., Israel, and Iran would likely compress near‑term risk premia, pulling down the front and belly of the curve as markets reprice stability. The front end looks anchored near policy, while the long end continues to embed term premium and inflation uncertainty. This is no longer a market paying you to simply extend duration and wait.

From a portfolio perspective, the message from the curve is fairly clear. The 5 to 7-year sector stands out as the most efficient place to take risk. It offers meaningful yield and roll-down without the policy sensitivity of the front end or the term premium and fiscal risks that dominate the long end.

This doesn’t look like a recession curve, nor a clean reflation story. Instead, it reflects a messy equilibrium: modest growth, persistent inflation risk, and central banks constrained by uncertainty. In that environment, curve positioning and relative value matter more than outright duration bets.